Did you know that Florida law mandates a $0 deductible for windshield replacements if you carry comprehensive insurance? Florida Statute §627.7288 ensures you don't have to pay out of pocket to restore your vehicle's safety. Dealing with confusing insurance terms and avoiding aggressive "parking lot" solicitors can feel overwhelming. You deserve a clear path to a safe vehicle without the headache of hidden fees or legal traps.

This guide explains how to file an auto glass insurance claim Florida drivers can use to secure a professional windshield replacement with no out-of-pocket costs. You'll learn how the 2023 legal reforms protect you from fraud while maintaining your right to quality service. We also explain why ADAS recalibration is a non-negotiable safety step for the 90% of new vehicles equipped with modern sensors. We cover the essential steps to ensure your safety tech works perfectly and your claim remains compliant with state law. It's time to get back on the road with confidence and a clear view.

Key Takeaways

- Understand how Florida Statute §627.7288 allows drivers with comprehensive coverage to receive windshield services without paying a deductible.

- Learn the critical differences between comprehensive and collision policies to determine if your vehicle qualifies for a $0 out-of-pocket replacement.

- Discover why ADAS recalibration is a mandatory safety requirement for modern vehicles and how it integrates with your auto glass insurance claim Florida.

- Master the step-by-step process of filing a claim, from gathering your VIN to choosing a qualified glass specialist who handles the paperwork.

- Identify common "parking lot" scams and learn why accepting cash incentives for glass work can jeopardize your insurance standing and vehicle safety.

Understanding Florida Statute §627.7288 and Your Rights

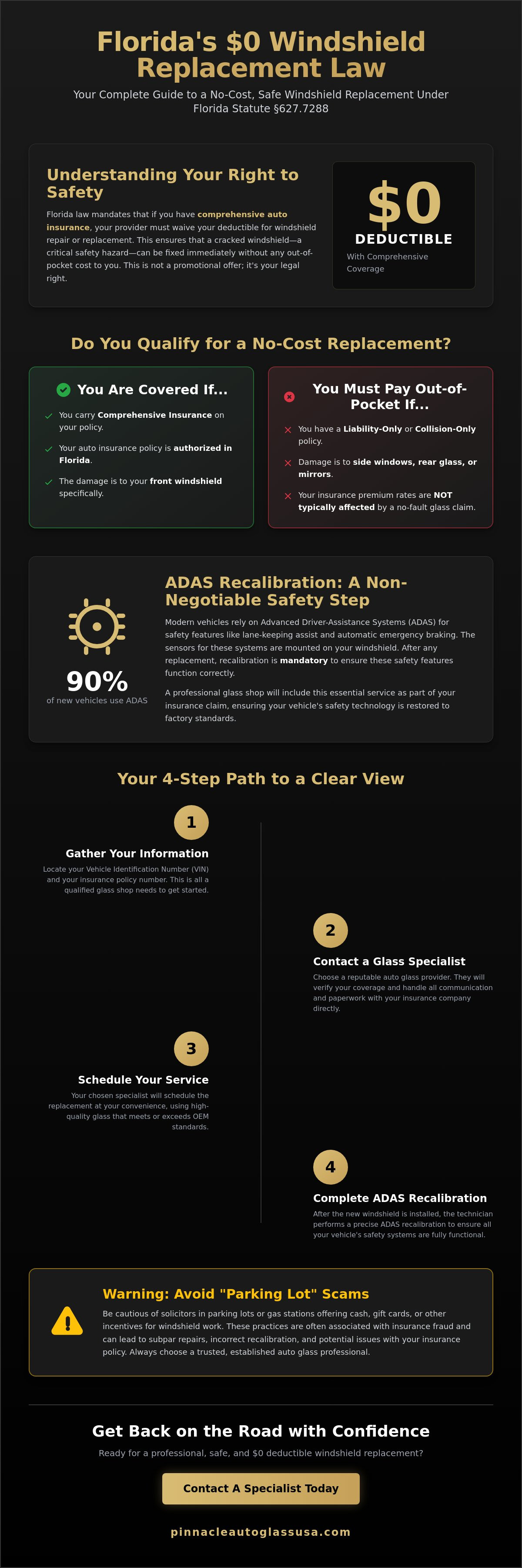

Florida's unique legal environment makes windshield safety a top priority for every driver. Florida Statute §627.7288 is the specific law that protects your wallet when road debris strikes. It mandates that any motorist with comprehensive coverage can receive a windshield repair or replacement with a $0 deductible. Insurers are legally prohibited from charging you a deductible for this specific service. This law applies strictly to vehicles insured within the state of Florida. It's designed to ensure that a cracked windshield, which is a major safety hazard, is fixed immediately without financial hesitation.

Many drivers hesitate to file an auto glass insurance claim Florida because they fear their premiums will spike. In reality, glass damage is typically considered a "no-fault" incident. By Understanding No-Fault Coverage, you can see how these claims differ from at-fault collisions. Most carriers don't raise rates for a single glass claim because it's a safety-related maintenance issue rather than a reflection of driving behavior. Recent 2023 legal reforms have also streamlined this process by prohibiting the Assignment of Benefits (AOB). You now work directly with your insurer and a professional glass shop, ensuring the claim stays transparent and efficient.

The Zero-Deductible Advantage

Clear visibility is a critical public safety measure. Florida's high-speed highways and frequent road debris make windshield damage common. The law removes the financial barrier to essential safety repairs, allowing you to prioritize your family's safety. This benefit applies specifically to the windshield, which is the primary structural component of your car's cabin safety. Note that side windows and back glass are usually subject to your standard deductible; the $0 mandate is reserved for the windshield alone. Choosing a professional shop ensures that your auto glass insurance claim Florida is handled correctly from the start.

Who Qualifies for No-Cost Replacement?

Eligibility depends on your specific insurance policy and the nature of the damage. You must meet the following criteria to qualify for a $0 deductible replacement:

- Comprehensive Coverage: You must have comprehensive insurance or "combined additional coverage" on your policy.

- Florida-Authorized Policy: Your insurance carrier must be authorized to provide coverage in the state of Florida.

- Specific Damage: The claim must be for the front windshield specifically, not other glass components.

Liability-only policies don't include this benefit. If you only carry the state-mandated minimum coverage, you'll likely have to pay the full cost of the replacement out of pocket. It's always best to verify your policy details before scheduling service. A reputable glass specialist can often help you confirm your coverage levels during the initial consultation.

Determining Your Eligibility for a Zero-Deductible Claim

Before you schedule any glass service, you must confirm your specific insurance benefits. Not every policy includes the same protections, even in a state with favorable glass laws. You can find these details on your insurance "Declaration Page," which is usually the first page of your policy document. Look for the section labeled "Comprehensive" or "Other Than Collision." If this coverage is active, you are eligible to file an auto glass insurance claim Florida under the state's zero-deductible mandate. This document clearly lists your deductibles for different types of incidents, but the windshield remains an exception for those with the right coverage.

Florida law is very specific about which policies qualify for the waiver. Per Florida Statute §627.7288, the deductible waiver applies specifically to the comprehensive portion of your auto insurance. If you only carry liability insurance, which only covers damage you cause to others, you won't have the coverage necessary for a $0 windshield replacement. Collision coverage also differs; it applies to accidents involving other vehicles or objects. For glass damage caused by road debris or unknown factors, comprehensive insurance is the mandatory trigger for the $0 out-of-pocket benefit.

Comprehensive vs. Liability Coverage

Comprehensive insurance is designed to cover events outside of your control. This includes theft, fire, and falling objects like rocks or road debris. Because Florida prioritizes road safety and clear visibility, this coverage triggers the legal requirement for insurers to waive your deductible. If you aren't sure about your current status, a quick check of your insurance company's mobile app can clarify your eligibility immediately. Drivers with liability-only policies will likely be responsible for the full cost of the service, as these policies don't cover damage to the policyholder's own vehicle.

Assessing the Damage: Repair or Replace?

Determining whether you need a repair or a full replacement is a critical next step. Most industry standards allow for a professional repair if the chip is smaller than the size of a quarter and not in the driver's direct line of sight. Repairs are fast and help maintain the structural integrity of the original glass. However, if the crack is longer than a few inches or has "spider-webbed" across the surface, a replacement is necessary. Modern vehicles with advanced safety systems often require a professional windshield replacement to ensure all safety features function as intended.

Don't ignore small chips. The intense Florida heat and vibrations from highway driving can turn a minor nick into a dangerous crack within hours. Addressing damage early often saves the original factory seal and prevents the need for a total replacement. If the damage has already spread across your field of vision, you should view your replacement options to restore your vehicle to factory standards. Filing an auto glass insurance claim Florida ensures that your view remains clear and your vehicle remains safe without the burden of an unexpected bill.

Why ADAS Recalibration is Mandatory for Modern Claims

Modern windshields are no longer just sheets of glass. They serve as the primary lens for your vehicle's Advanced Driver Assistance Systems (ADAS). These systems include critical safety features like automatic emergency braking, lane-keeping assist, and adaptive cruise control. When you initiate an auto glass insurance claim Florida, the process must include more than just a physical glass swap. It requires a precise electronic reset of the cameras and sensors mounted behind your rearview mirror. These components "see" through the glass to monitor the road ahead. If the camera is even a fraction of a millimeter out of alignment after a replacement, your safety systems may fail to react correctly in an emergency.

The legal framework in the state supports this comprehensive approach to safety. Under Florida Statute §627.7288, insurers must restore your vehicle to its pre-loss condition. For vehicles manufactured after 2020, where over 90% of new models feature at least one ADAS component, "pre-loss condition" includes a fully functioning safety suite. Most insurance carriers now recognize recalibration as a standard and necessary part of the replacement invoice. Skipping this step isn't just a technical oversight; it's a significant safety risk that can lead to unexpected braking or steering corrections.

The Link Between Glass and Vehicle Safety Tech

Cameras and sensors are calibrated to the specific thickness and clarity of factory-standard glass. Even minor glass imperfections or a slight shift in the mounting angle can distort the sensor's field of vision. This distortion causes the vehicle's computer to miscalculate the distance to the car in front of you or misidentify lane markings. Because these systems are integrated into the windshield, a new installation breaks the original factory calibration. Professional glass shops use specialized diagnostic tools to ensure the camera's "eye" is perfectly centered and focused. This ensures your auto glass insurance claim Florida results in a vehicle that is as safe as the day it left the showroom.

Static vs. Dynamic Recalibration

Depending on your vehicle's make and model, technicians will perform one of two types of recalibration. Static recalibration occurs in a controlled shop environment using specialized targets and lasers to align the sensors. Dynamic recalibration requires a technician to drive the vehicle at specific speeds on well-marked roads to allow the system to "learn" its surroundings. Many modern vehicles require both types of calibration to achieve full system integrity. A qualified specialist will handle these technical requirements as part of the standard claim process. This ensures every safety sensor is verified and functional before you get back behind the wheel.

Filing Your Auto Glass Claim: A Step-by-Step Guide

Filing an auto glass insurance claim Florida is a straightforward process when you work with the right professionals. Many drivers mistakenly call their insurance agent first. This often leads to unnecessary delays or being routed through a third-party claims network. Instead, you should contact a qualified specialist like Pinnacle Auto Glass as your first step. A professional shop understands the specific billing requirements of Florida insurers and can manage the communication for you. This ensures the claim is filed accurately and that all safety requirements, including ADAS recalibration, are documented correctly from the start.

Once you've selected a provider, the process follows a logical sequence to get you back on the road safely:

- Step 1: Contact the Specialist. Reach out to your glass shop to initiate the process. They will act as your guide through the insurance paperwork.

- Step 2: Provide Documentation. You'll need your insurance policy number and your Vehicle Identification Number (VIN).

- Step 3: Schedule Service. Choose between a mobile appointment or an in-shop visit based on your vehicle's tech requirements.

- Step 4: Claim Verification. The glass shop verifies your $0 deductible eligibility and files the claim directly with your carrier.

- Step 5: Final Inspection. Confirm the installation is clean and that any necessary safety sensor recalibrations are successfully completed.

Gathering Necessary Information

Your VIN is the most important piece of data for a modern auto glass insurance claim Florida. This 17-digit code allows the shop to identify the exact glass specifications for your vehicle, including integrated rain sensors, heating elements, or ADAS camera brackets. You should also note the specific date the damage occurred and the cause, such as a rock strike on the interstate. Having your insurance carrier's name and policy effective dates ready will prevent administrative delays. These details ensure that the replacement glass matches your vehicle's original factory equipment perfectly.

What to Expect During the Process

Most professional shops use a "direct billing" system. This means the glass company sends the invoice directly to your insurance carrier. Under Florida law, if you have comprehensive coverage, you should never be asked to pay a technician at the time of service. Claim approval is usually instantaneous, and most installations are completed within a few hours. After the glass is set, the technician will perform the required safety system resets. If you are ready to begin the process, contact us today to start your claim and schedule your professional windshield replacement.

Selecting an Expert Provider for Your Florida Glass Claim

Choosing the right partner for your auto glass insurance claim Florida is the final step in restoring your vehicle's safety. A windshield is a critical structural component of your car. It supports the roof during a rollover and ensures proper airbag deployment. Using high-quality glass and professional-grade adhesives is essential for these safety systems to function correctly. You need a provider that treats your vehicle with technical precision rather than just another transaction. A shop that specializes in both glass and ADAS recalibration is no longer a luxury; it's a safety requirement for modern driving. We ensure every technical specification is met before you get back on the road.

Professional certification matters because it dictates the quality of the bond between the glass and your vehicle's frame. High-quality urethanes require specific curing times to reach their full strength. Rushing this process or using inferior materials can lead to leaks or even the glass detaching during a collision. By selecting an authoritative expert, you ensure that your replacement meets or exceeds the original manufacturer standards. This attention to detail protects your investment and provides peace of mind for you and your passengers.

Spotting and Avoiding Glass Scams

Florida's zero-deductible law has historically attracted predatory "parking lot" solicitors. These individuals often approach drivers at gas stations or car washes with unsolicited offers for a "free" windshield. A common warning sign is the "Free Gift" trap. They might offer cash, gift cards, or other incentives to convince you to file a claim. Under the 2023 legal reforms, auto glass companies are strictly prohibited from offering rebates or items of value in exchange for making an insurance claim. Accepting these offers puts you at risk of participating in insurance fraud. Poor-quality installations from these transient operations often lead to wind noise, water damage, or catastrophic failure. Always choose an established business with a reputation for technical excellence and legal compliance.

The Pinnacle Auto Glass Difference

We prioritize your safety and convenience by managing every aspect of the repair process. Our team handles direct insurance billing to simplify the customer experience. You won't have to navigate the complexities of the auto glass insurance claim Florida process alone. We provide comprehensive expertise in both windshield replacement and ADAS recalibration for all vehicle makes and models. This dual-specialization ensures your safety cameras are perfectly aligned and tested before you leave our care. We use industry-leading materials and follow strict manufacturer specifications to maintain your vehicle's integrity. Don't settle for a "quick fix" that ignores your car's advanced technology and safety requirements.

Start your Florida auto glass claim with Pinnacle Auto Glass today.

Restore Your Visibility and Safety Today

Florida laws are designed to keep you safe by removing the financial burden of windshield damage. By exercising your right to a zero-deductible replacement, you ensure your vehicle remains structurally sound and your vision remains clear. Modern safety features require more than just new glass. Expert ADAS recalibration is a critical step to keep your lane-keeping and emergency braking systems functioning as the manufacturer intended.

Managing an auto glass insurance claim Florida doesn't have to be a complicated task. Our team provides professional mobile service and handles direct insurance billing to save you time. We focus on technical precision and legal compliance so you can avoid the risks of predatory scams. It's time to prioritize your vehicle's safety with a partner you can trust. We're ready to assist you with every step of the process to ensure your car is restored to factory standards.

File Your Zero-Deductible Florida Glass Claim Now

Frequently Asked Questions

Is windshield replacement really free in Florida?

Yes, windshield replacement is effectively free for Florida drivers who carry comprehensive insurance. Florida Statute §627.7288 requires insurers to waive the deductible for windshield repairs or replacements. This law ensures that financial concerns don't prevent you from fixing a safety hazard. If you have the correct policy, you'll pay $0 out of pocket for the service.

Will filing a windshield claim increase my insurance premiums in Florida?

Filing a glass-only claim typically does not increase your insurance premiums. Most carriers treat these as no-fault incidents because they are often caused by road debris or weather. Since 2024, litigation rates for glass claims have dropped significantly, helping stabilize the market. You should check your specific policy, but safety-related glass repairs are usually protected from rate hikes.

Do I have to use the repair shop my insurance company recommends?

You have the legal right to choose any repair shop in Florida. Insurance companies often have "preferred providers," but you aren't required to use them. It's often better to select a specialist who can handle both the physical glass installation and the complex ADAS recalibration required for modern vehicles. Choosing your own shop ensures you receive the quality of glass and service you expect.

How long does the insurance claim process take for a new windshield?

The administrative side of an auto glass insurance claim Florida is often completed in minutes. Once you provide your VIN and policy information, the shop can verify coverage almost instantly. The physical replacement and safety tech recalibration usually take about two to four hours. This timeline allows the adhesive to bond correctly and the safety sensors to be precisely aligned.

What happens if I don't recalibrate my cameras after a windshield replacement?

Skipping recalibration can cause your vehicle's safety features to operate incorrectly or stop working. Cameras mounted to the windshield provide the "vision" for lane-keeping and emergency braking systems. If these aren't reset to factory specifications, the car might miscalculate the distance to other vehicles. This technical failure increases your risk of a collision and compromises your safety on the road.

Does the Florida zero-deductible law cover side windows or sunroofs?

Florida's zero-deductible law applies only to the front windshield. Side windows, rear glass, and sunroofs aren't included in the mandate. If these components are damaged, you'll likely have to pay your standard comprehensive deductible. This distinction exists because the windshield is considered a primary safety and structural component that is essential for clear visibility while driving.

Can I file a claim if I only have liability insurance?

You cannot file a $0 deductible claim with a liability-only policy. Liability insurance only covers damage you cause to other people or their property. To access the benefits of the Florida glass statute, you must have comprehensive coverage on your policy. If you carry the state minimums, you'll be responsible for the full cost of the replacement or repair.

What should I do if a glass company offers me cash to replace my windshield?

You should report the offer and find a different service provider. It's now illegal in Florida for glass shops to offer cash, gift cards, or incentives in exchange for an auto glass insurance claim Florida. These practices were banned in 2023 to combat fraud and rising premiums. Legitimate, professional shops focus on quality installation and safety rather than providing illegal kickbacks.