Paying out of pocket for a cracked windshield might seem like the smartest way to avoid a complex insurance headache. However, with 85% of 2026 vehicles now featuring integrated safety sensors, a basic glass swap is rarely a simple fix. You are likely asking, does car insurance cover windshield replacement, or will filing a claim just lead to higher premiums and more confusion?

It is normal to feel overwhelmed by deductibles and policy jargon. You want your vehicle returned to safety standards quickly without facing unexpected costs or long delays. We understand that your priority is a safe, functional vehicle and a clear understanding of your financial responsibility. This guide explains exactly how your coverage works, including the mandatory ADAS recalibration required for modern automotive glass.

We will show you how to identify if your specific damage qualifies for a no-deductible repair or a full replacement. You will also learn the most efficient way to handle your insurance claim to ensure your high-tech safety systems are properly restored. From understanding comprehensive coverage to managing your deductible, this is your roadmap to a clear view of the road ahead.

Key Takeaways

- Identify whether comprehensive or collision coverage applies to your specific damage to ensure your claim is processed correctly.

- Determine if your policy does car insurance cover windshield replacement through a zero-deductible glass benefit or requires a standard out-of-pocket payment.

- Evaluate the financial "break-even" point by comparing simple glass costs against the expense of mandatory ADAS recalibration for modern vehicles.

- Learn the essential steps for documenting glass damage and verifying the scope of work before you contact your insurance provider.

- Ensure your vehicle meets original safety standards by choosing a provider that handles both complex insurance paperwork and technical safety system resets.

Understanding When Car Insurance Covers Windshield Replacement

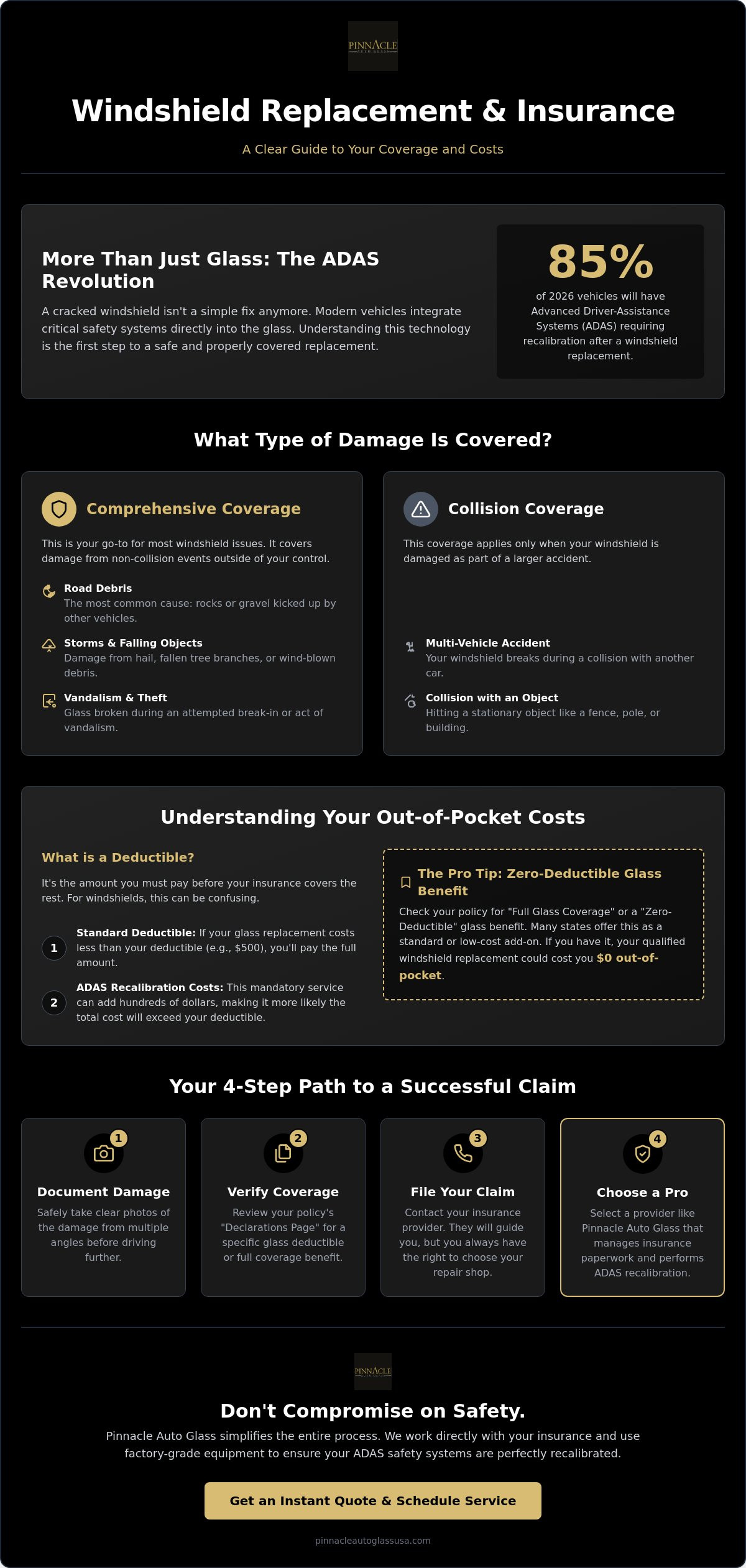

Determining if your policy pays for glass damage starts with your specific coverage type. For most drivers, the answer to does car insurance cover windshield replacement depends on having comprehensive coverage. This specific portion of your Vehicle insurance policy handles damage caused by events outside of your control. If you only carry liability insurance, your provider will not pay for your own glass repairs. Liability only covers damage you cause to other people or their property.

Insurance companies generally categorize glass claims into two groups: glass-only claims and accident-related claims. A glass-only claim usually involves a single piece of glass damaged by a specific, isolated event. An accident-related claim occurs when the windshield is broken as part of a larger collision. Identifying which category your damage falls into is the first step toward a successful claim process.

Comprehensive vs. Collision: Which Applies to You?

Comprehensive coverage is the industry standard for the majority of glass claims. It covers non-collision events like theft, vandalism, and falling objects. Many drivers find it confusing that a rock flying off a truck is considered a comprehensive claim. Even though your car is moving, the rock is treated as a flying object rather than a collision with another vehicle. Collision coverage only triggers if your windshield breaks during a multi-vehicle accident or if you hit a stationary object like a fence or a pole. If the glass is the only thing broken, you are almost always filing under your comprehensive policy.

Common Scenarios for Covered Glass Damage

Standard policies typically cover several specific types of glass damage that occur during daily driving. These include:

- Storm damage: This includes impact from fallen tree branches, hail, or debris carried by high winds during severe weather events.

- Vandalism and theft: If a person smashes your windshield or side windows during an attempted break-in, insurance usually covers the replacement.

- Road debris: This is the most frequent cause of damage. Small stones or gravel kicked up by other vehicles create chips that can quickly spread.

- Spontaneous cracks: Extreme temperature fluctuations can cause a tiny, pre-existing chip to expand rapidly across the glass surface.

Insurance providers prioritize safety and often prefer to cover a small repair immediately. This prevents the higher cost of a full replacement later. However, if a crack is in the driver's line of sight or exceeds the size of a credit card, a full replacement is required. Modern vehicles with safety sensors require more than just new glass; they need precise recalibration to keep those systems functional. We ensure these technical requirements are met so your vehicle remains safe on the road.

Deductibles and the Zero-Deductible Glass Benefit

A deductible is the specific amount you agree to pay out of pocket before your insurance provider covers the remaining costs of a claim. While comprehensive auto insurance generally includes glass protection, your standard deductible often applies. If you have a $500 or $1,000 deductible, you might find that the cost of a standard piece of glass is lower than your out-of-pocket requirement. This leads many drivers to wonder, does car insurance cover windshield replacement in a way that actually provides financial relief? The answer often depends on whether you have a "Full Glass Coverage" or "Zero-Deductible" endorsement added to your policy.

This endorsement is a specific rider that removes the deductible requirement for glass-only claims. It ensures that if a rock hits your windshield, you pay nothing for the replacement or repair. Even without this rider, many insurance companies prioritize safety by waiving the deductible for a windshield repair. They would rather pay for a small resin injection now than a full replacement later. Checking your "Declarations Page" is the fastest way to see if you have a separate, lower deductible specifically for automotive glass.

How Your Deductible Affects Out-of-Pocket Costs

Your financial strategy changes based on the technology in your vehicle. For an older car with basic glass, a replacement might cost less than a $500 deductible. In that scenario, filing a claim doesn't make sense. However, modern vehicles with Advanced Driver-Assistance Systems (ADAS) are a different story. These windshields require precise recalibration of cameras and sensors. Because this technical work increases the total invoice, the cost will almost always exceed a standard deductible. We recommend that you review your policy details with a professional to determine the most cost-effective path forward for your specific vehicle year and model.

States with Mandatory No-Deductible Glass Laws

Several states view a clear, intact windshield as essential safety equipment and have passed laws to reflect that. Currently, Florida, Kentucky, and South Carolina require insurers to provide $0 deductible windshield replacements for policyholders with comprehensive coverage. This means you won't pay a cent for the glass or the labor. Other states, including Arizona, Connecticut, Massachusetts, Minnesota, and New York, require insurance carriers to offer optional full glass coverage with no deductible.

Legal requirements can change, and it's important to stay informed about local shifts. For example, South Carolina is currently reviewing Bill H. 4817, which could move the state toward an optional zero-deductible model by 2027. If you don't live in a mandatory state, adding a glass endorsement is usually a very inexpensive way to protect yourself from the high costs of modern glass technology. It provides peace of mind, knowing that a single piece of road debris won't result in a large, unexpected bill.

Deciding Between Filing a Claim or Paying Out-of-Pocket

Choosing between an insurance claim and a cash payment requires a clear look at your total liability. If you have comprehensive insurance for windshield damage, you have the option to let your provider handle the bill. However, the financial logic shifts based on your deductible and the technology in your car. While does car insurance cover windshield replacement is a common question, the more important inquiry is whether filing that claim is the most cost-effective move for your specific vehicle.

For older vehicles with basic glass, paying out-of-pocket might save you the trouble of a claim if the cost is near your deductible. For modern vehicles, the "break-even" point is much higher. Using your insurance often makes more sense when the repair involves complex safety systems. Beyond the immediate cost, remember that a professional, insurance-backed replacement creates a formal service record. This documentation proves you maintained the vehicle to high safety standards, which can be a selling point for future resale.

Evaluating the Total Cost of Replacement

The primary factor in your decision is the complexity of your vehicle's glass. You need to understand how much does windshield replacement cost in 2026 before making a choice. For a standard sedan without sensors, the price might be relatively low. For modern cars, the total invoice includes several critical components:

- High-quality automotive glass designed for your specific model.

- Professional labor for a leak-free installation.

- Mandatory ADAS recalibration to ensure safety cameras and sensors function correctly.

We recommend getting a detailed quote before contacting your agent. If the total invoice is significantly higher than your deductible, filing a claim is the logical choice. This is especially true for the 85% of 2026 vehicles that require technical recalibration as part of the glass service.

Will a Glass Claim Raise Your Insurance Premium?

A common fear is that a single claim will spike your monthly rates. In most jurisdictions, comprehensive glass claims are considered "no-fault" events. Insurance companies generally don't raise premiums for a single instance of road debris or storm damage because these events are outside your control. The primary risk is "frequency." If you file multiple glass claims within a 12-month window, your carrier might re-evaluate your risk level. This could lead to a rate adjustment or the loss of a "claims-free discount." It's a good idea to check your current discount status with your agent before you finalize the claim process.

How to Successfully Navigate an Auto Glass Insurance Claim

Filing a claim for glass damage shouldn't be a source of stress. While does car insurance cover windshield replacement is the initial hurdle, knowing how to manage the paperwork ensures you aren't stuck with unexpected bills. Start by documenting the damage immediately. Take clear, close-up photos of the impact point and a wide shot of the entire windshield to show the location of the crack. This evidence is vital for your adjuster.

Contact your glass specialist before calling your insurance company. We can verify the technical scope of work and provide an accurate estimate that includes all necessary safety steps. You should also confirm whether your policy covers Original Equipment Manufacturer (OEM) glass. Some policies default to aftermarket glass unless you have a specific endorsement. Finally, ensure the shop is part of your insurance carrier's approved network to simplify the billing process and reduce administrative delays.

Step-by-Step Guide to Filing Your Claim

Once you have your documentation, follow these steps to move the process forward efficiently:

- Call your glass specialist to obtain a detailed estimate and technical specifications for your vehicle.

- Provide your policy number and the date the damage occurred to your insurance carrier's claims department.

- Request that your insurance company works directly with the glass shop for billing to avoid reimbursement delays.

Handling the technical details upfront prevents the insurance company from questioning the necessity of specific line items later. If you need help starting this process, contact our team for assistance with your insurance claim.

Why ADAS Recalibration Must Be Included in the Claim

Modern insurance contracts are designed to return your vehicle to its pre-loss safety condition. This means your claim must include ADAS calibration auto glass services. If your vehicle features lane-keep assist, automatic emergency braking, or adaptive cruise control, those systems rely on cameras mounted to the windshield. Insurance companies are contractually obligated to pay for these resets as part of the restoration process.

A standard windshield replacement without recalibration leaves these safety features non-functional or dangerously inaccurate. Avoid "glass-only" shops that lack the specialized equipment to perform these technical resets. Ensure your insurance adjuster approves recalibration as a mandatory line item. This guarantees your vehicle meets original safety standards before it returns to the road.

Choosing Pinnacle Auto Glass for Your Insurance-Backed Replacement

Managing a claim shouldn't take up your entire day. While you now know the answer to does car insurance cover windshield replacement, the next step is finding a partner who executes the technical work and the administrative tasks with equal precision. We position ourselves as that partner by combining nationwide reach with the dedicated attention of a local specialist.

Our capabilities extend across the country; we offer both mobile and in-shop services to fit your schedule. We understand that your vehicle's safety depends on the quality of the materials used. We only install glass that meets or exceeds original safety standards. This ensures structural integrity and provides optimal clarity for your safety sensors.

We Handle the Paperwork for You

Our team coordinates directly with all major insurance carriers to streamline your experience. We manage the technical specifications and documentation required by adjusters, allowing for a hassle-free billing process. We talk to the insurance company so you don't have to. For business owners, we provide specialized support for fleet glass services and commercial truck glass claims. We ensure that your commercial insurance requirements are met so your vehicles return to service without unnecessary downtime.

Quality Standards and Safety Guarantee

Safety is our non-negotiable priority. Every technician on our team is an expert in the nuances of modern automotive glass. Because 85% of 2026 vehicles feature integrated safety systems, we perform mandatory ADAS recalibration on every applicable job. We don't consider a replacement complete until we verify that your lane-keep assist and emergency braking systems are fully functional. This rigorous approach prevents safety system failures that can occur when recalibration is ignored.

We provide a professional installation that respects both your time and your vehicle's complex engineering. Our goal is to act as your dependable guide through the entire restoration process. Contact Pinnacle Auto Glass today to start your stress-free insurance replacement and get back on the road with total confidence.

Secure Your Safety and Restore Your View

Navigating the details of your automotive policy doesn't have to be a burden. You now understand how comprehensive coverage functions and why the technical complexity of modern glass makes insurance claims a logical financial choice. While the question of does car insurance cover windshield replacement is common, the priority is ensuring your vehicle returns to its original safety specifications with minimal stress.

Our team is here to guide you through every step. We provide expert ADAS recalibration with every replacement and coordinate direct insurance billing for a completely hassle-free experience. With nationwide service for both personal and commercial vehicles, we ensure high-quality results regardless of your location. It's our mission to get you back on the road with a clear view and fully functional safety systems.

Get a Professional Quote and Start Your Claim with Pinnacle Auto Glass today. Take the next step toward a safer drive with a partner you can trust.

Frequently Asked Questions

Is it better to pay for a windshield out of pocket?

Paying out of pocket is only beneficial if the total cost of the glass and labor is less than your comprehensive deductible. For the 85% of 2026 vehicles that feature ADAS technology, the technical recalibration costs often push the total invoice well above a standard deductible. In these cases, using your insurance is the more cost-effective choice for restoring your vehicle's safety systems.

Does insurance cover a cracked windshield if I only have liability?

No, liability-only policies do not cover your own vehicle's glass damage. Liability insurance is designed to pay for repairs to other people's property if you are at fault in an accident. To protect your own windshield from road debris, hail, or vandalism, you must carry comprehensive coverage on your policy. This is the primary way does car insurance cover windshield replacement for your own car.

Will my insurance premium go up if I replace my windshield?

Most insurance carriers will not raise your premium for a single comprehensive glass claim. These are generally considered "no-fault" events because road debris and storm damage are beyond your control. However, filing multiple claims in a short period can lead to a risk re-evaluation. It's best to check your "claims-free discount" status with your agent before finalizing a new claim.

How do I know if my insurance covers windshield replacement with OEM glass?

You can determine if your policy covers OEM glass by reviewing your insurance declarations page or contacting your agent directly. Many standard policies utilize high-quality aftermarket glass to manage costs. If you prefer parts from the original manufacturer, verify if you have an "OEM endorsement" added to your coverage. This specific rider ensures the insurance company pays for the higher cost of original parts.

Do I have to pay my deductible for a windshield chip repair?

Most insurance providers waive the deductible for a windshield chip repair. They prefer the lower cost of a resin-based repair over the high expense of a full replacement. This policy encourages drivers to fix small chips before they expand into larger, more dangerous cracks. It's a proactive way for insurers to save money while keeping your vehicle safe and structurally sound.

What happens if my insurance company refuses to pay for ADAS recalibration?

Insurance companies are contractually obligated to return your vehicle to its pre-loss safety condition. Since ADAS recalibration is a manufacturer-required safety step, it is a covered expense under most comprehensive policies. If they refuse, provide a technical statement from your glass specialist. This documentation explains the necessity of the reset for safety systems like emergency braking and lane-keep assist.

Can I choose my own glass shop or must I use the one insurance recommends?

You have the legal right to choose any glass shop for your replacement in the majority of states. While your insurance company may suggest a specific "preferred provider" or network shop, you are not required to use them. Selecting a shop that specializes in both glass and ADAS recalibration ensures your vehicle meets all modern safety standards after the installation is complete.

How long do I have to file a glass claim after the damage occurs?

You should file your glass claim as soon as possible, though most policies allow for a window of 30 to 90 days. Waiting too long can allow a small chip to spread across the entire surface. This makes the repair more expensive and could lead the insurance company to question the timeline of the damage. Prompt action ensures your vehicle's structural integrity is restored quickly.